Gallium, The High-Impact Rare Earth

Technological metals are often called as such due to their outstanding physical properties. This is, for example, the case with the extreme resistance of metals such as titanium or tungsten (follow the links for the associated investment report).

Others are unique because of their electrochemical properties. This is the case for gallium, a rare earth metal essential in the production of electronics.

It is crucial in the production of LEDs, as well as a whole array of specialized semiconductor components, making it a crucial part of the supply chain for not only the tech industry but also aerospace, defense, and strategic interests.

Gallium is also a metal at the center of the USA-China trade wars, with escalating sanctions that could disrupt Western producers. With its prices reaching highs not seen in more than a decade, it is a potentially valuable element worth paying attention to for investors.

Gallium Description

Gallium is a rare earth element that makes up just 19 parts per million of the Earth’s crust. It is commonly a silvery-white metal.

It is almost never present in pure form in nature but as elemental traces in other metallic ores. As a result, gallium production is almost entirely the result of refining more common metals, mostly aluminum, although it can also be produced from sulfidic zinc ores and historically was even produced from special types of coal.

Gallium is a remarkable metal with a low melting point of 29.8 °C (85.6 °F), meaning it will melt in a person’s hands.

Source: Nanographi

Its boiling point is very high (2,400°C), making it mostly liquid in most conditions. It is generally nontoxic except for some rare chemical forms.

Due to its rarity and sourcing as a by-product, global gallium annual production is very small and grew from just a few tons/year in the 1970s to 450 tons/year in 2024.

Gallium Market

Gallium is a very small market, worth only $25M in 2023, but it is expected to grow at a 7% CAGR until 2030.

The largest part of the market is for integrated circuits (IC) applications, with optoelectronics (LEDs, laser, etc.) most of the rest.

Source: GrandView Research

Gallium is currently at a 13-year high, following export restrictions by China (more on that below).

Source: Mining.com

Gallium Applications

Electronics Manufacturing

Gallium’s main and most critical application is in semiconductors, with several different chemical forms.

Gallium arsenide is used in electronic circuits: microwave, high-speed switching circuits, and infrared. It is also used for low-energy red LED lights, while gallium phosphide is used for green LEDs.

Gallium nitride is the “miracle component” used to produce blue LEDs, a Nobel Prize-winning technology, essential for the now omnipresent white light LEDs, and important in indoor farming, water purification (UV-LEDs), Blu-Ray data storage, and surgical blue lasers.

Gallium works in semiconductors by “doping” the material, improving its energy level. This method works with gallium and other rare elements like boron or antimony.

Source: Wikipedia by VectorVoyager

Gallium antimonide, mixed with the chemical antimony, is also used for infrared detectors, LED & laser, and thermophotovoltaic systems (increasingly used in heat batteries).

(you can read more about investing in antimony in “Chinese Restrictions on Antimony Exports Highlight The Strategic Importance of this Metalloid”)

It should be noted that while gallium nitride is important in many semiconductor applications, it is especially strategically important in LED and laser-related applications. This includes LIDAR (laser radar) for autonomous vehicles and robotics.

Gallium could also become important for flexible electronics, as its flexibility, low toxicity, and liquid phase at low temperatures without evaporation make it perfect for this application.

Renewable Energy

Gallium arsenide and nitride are used in photovoltaic cell tunnels as a p-dopant, as well as solar micro-inverters, optimizers, and energy storage systems and in thin-film solar cells that combine gallium with indium, copper, and selenium (CIGS).

Medical

As previously mentioned, gallium is important for surgical blue-light lasers.

Gallium is occasionally used in medical imaging and cancer therapies (nuclear medicine), notably its gallium-67 and gallium-68 isotopes.

Source: Transparency Market Research

Gallium-based liquid metal nanoparticles also display antibacterial activities and could help fight bacterial antibiotic resistance.

Aerospace

Gallium nitride is inherently radiation tolerant, unlike silicon. This makes it a good choice for producing electronics in high-radiation conditions, like space. As a result, the material is crucial for satellite manufacturing, used in a large variety of key components:

- Ion thrusters, to convert power from the satellite solar panels

- High-precision BLDC motors for driving the reaction wheels used by small CubeSats

- Robotics and automated instrumentation used in space missions

- LIDAR for distance measurement.

China’s Control Of Gallium Supply

New Sanctions

In 2023, China started restricting gallium and other rare earth exports. This had already pushed prices up and caused a panic among semiconductor manufacturers with operations in China.

As China accounts for the immense majority of global gallium production (98.8%), this is essentially going to starve semiconductor manufacturers of the crucial element.

A new set of rules regarding export restrictions is creating even more strict limitations. Notably, this could prohibit foreign companies and countries from helping US manufacturers to evade the controls. For example, reprocessing Chinese gallium and reselling it to the US would be strictly forbidden, and ignoring this rule could lead to the loss of Chinese gallium shipment altogether for the “guilty” party.

This follows a similar move in antimony, that has triggered a price run on the element used in semiconductor and ammunition production.

Source: Mining.com

Part Of A Broader Chip War

This move in the US-China trade war is a retaliation against American tentatives to cripple the Chinese chip industry through a series of sanctions against the export of advanced chips and chip manufacturing equipment, first advanced EUV and then DUV machines.

In parallel, the US is trying to boost domestic production, with attempts to get Intel back on track and to get TSMC to move factories to Arizona.

Now, China is actively striking back in its own tentative to cripple the US chip manufacturing.

China said its ban on gallium and germanium was because of the minerals’ “dual military and civilian uses”. A phrasing that mimics exactly the same justification given by the USA for sanctioning Chinese firms, especially in the context of the war in Ukraine.

The move by China is likely to partially work, as gallium is an extremely small market, easy to monitor. The alternative currently existing suppliers are also unlikely to be of much help, as #2 and #3 are respectively Russia and Ukraine.

How Did China Become So Dominant

As gallium doesn’t exist independently, China’s dominance in the industry is mostly a by-product of its massive aluminum industry.

But even this presence does not explain it all. After all, China is producing “only” 59% of the world’s aluminum.

The difference is that China has mandated by law for its aluminum producers to recover gallium, something that otherwise would not at all be a priority for aluminum refineries.

This has created a surplus of gallium on the market for more than a decade, helped China build a stockpile, and lowered domestic prices while putting its competitors out of business.

An Expensive Mistake

In retrospect, Western governments made a clear mistake by ignoring vulnerability in critical materials like tungsten, antimony, and rare earth. This was an avoidable mistake, as experts in the industry and military have been warning about it for many years now.

Giving up “costly” stockpiles of strategic minerals, built during the Cold War, compounded the problem.

A report by the US Geological Survey (USGC) indicates the Chinese gallium ban could cost the US as much as $3.1B, with the associated ban on germanium as much as $0.4B.

Of course, the real cost could be much higher, as it also creates very real strategic and industrial vulnerability. This vulnerability could potentially impact the US’ ability to conduct military operations against China or its allies like Russia and, therefore, reduce its diplomatic options.

The same report indicates that gallium prices could go up by more than 150% and germanium prices up by 26% in the event of a total ban.

Solving Gallium Supply

As gallium needs to be extracted from existing industrial metallurgical processes, the only realistic alternative to Chinese aluminum smelters is non-Chinese aluminum producers.

Rio Tinto Group (RIO +0.16%) said it’s considering producing gallium from its Canadian aluminum operations.

Metlen Energy & Metals SA (MYTIL.AT) is exploring something similar in Greece, with Metlen the EU’s largest bauxite producer (the ore from which aluminum is extracted).

In the USA, Trafigura-owned Nyrstar is exploring a $150M germanium and gallium recovery and processing facility at its zinc smelter in Tennessee.

However, Western aluminum companies are looking for a long-term commitment from governments and/or semiconductor firms before taking the expensive steps of retrofitting their smelting operations to add a gallium extraction step.

It is unclear if the $29M to support gallium and germanium extraction earmarked by the US Defense Department will be enough.

Without such a safety net, they are unlikely to take the risk and could be exposed to a potential price crash if Chinese supply unexpectedly re-enters the market. After all, pre-sanctions gallium production was generally higher than total demand.

Gallium Companies

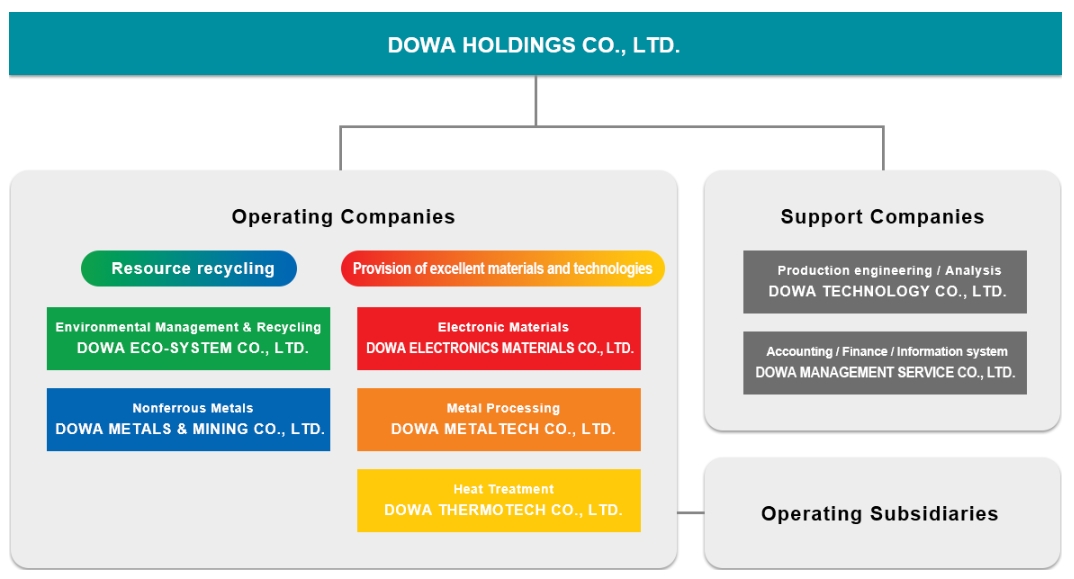

DOWA (5714.T)

While mostly dominated by China, there are some producers of gallium totally independent from it. One of them is the Japanese DOWA Metals and Mining Company, a part of the larger DOWA Holdings.

Source: DOWA

Gallium production is done through smelting of zinc imported from Mexico, and performed in Japan.

DOWA is primarily a recycling company, with a raw metal production side for zinc. This includes recycling of metals, but also batteries. It also performs the recycling of wastewater in Japan.

Source: DOWA

The company also supplies other materials for the semiconductor industry, notably infrared and ultraviolet LEDs made with gallium. So if Western markets are suffering from a shortage of such materials, this could strongly benefit DOWA, as it has already vertically integrated this very vulnerable part of the supply chain.

Source: DOWA

Like many industrial Japanese companies, its stock has been trading at rather low multiple for many years, with a P/E below 8 at the time of writing of this article. This can be seen as both a problem (value trap) or an opportunity depending on investors’ profile and time horizon.

Rio Tinto

Rio Tinto Group (RIO +0.16%)

Rio Tinto is the world’s second-largest mining company. The largest part of the company’s business is in iron ore. However, it is also a very large producer of copper and aluminum, with strong expansion plans for copper production.

As mentioned, it is considering getting into the gallium business as well, through its Canadian aluminum smelters (see below). This could provide investors exposure to the gallium sector, while also counting on much more established businesses in mining “mainstream” metal to carry on in any case.

Iron

Rio Tinto’s historical business was, and still is, centered around the Pilbara region in West Australia, renowned for its iron ore.

It is now engaging in a project that took more than 10 years to get off the ground, Simandou, in Guinea (Africa). Once complete, Simandou will be Africa’s largest mine and infrastructure project. The Simandou project is a joint venture between the Government of the Republic of Guinea, Rio Tinto, and Chinese Chalco Iron Ore Holdings (CIOH).

Rio Tinto is also looking at ways to reduce its iron carbon emissions, notably with BioIron, a proprietary technology tuned to Pilbara ore, using biomass and microwave to replace coal usage. This could reduce associated carbon emissions by 95%.

Source: Rio Tinto

(we explored in detail the case for investing in iron in a dedicated report)

Copper

Rio Tinto is quickly growing its copper production with the massive expansion of Oyu Tolgoi, the largest mine in Mongolia. The mine is currently ramping up to 500 ktpa (thousands of tons per year), with a target for 1,000 ktpa in the next five years.

Rio Tinto is expected to provide 25% of growth volumes in global copper supply in the next 5 years.

Rio Tinto is also a leader in the innovation of copper extraction through its venture Nuton, whose new technology allows for a much higher rate of copper recovery from mined ore.

Lithium

Rio Tinto is progressively becoming a giant of lithium production. The first step was the acquisition of the Ricon project in Argentina in 2021.

It was followed by the troubled Jadar lithium project in Serbia, which was canceled under strong pressure by local activists, but might restart after all.

However, the big change came with the acquisition of Arcadium Lithium in 2024, the 3rd largest lithium producer in the world, which was the result of the merger of Allken and Livent a year prior.

Source: Arcadium

This puts Rio Tinto at almost the top lithium company in the world in terms of reserves and total capacity.

Source: Rio Tinto

Regarding this acquisition, what has been described as “Rio Tinto’s real prize” is Arcadium’s direct lithium extraction (DLE) technology. Arcadium has been working on DLE since 1996, in combination with evaporation pounds, and recently made significant progress in making it commercially viable as a stand-alone extraction method.

Arcadium also developed LIOVIX, a form of printable lithium foil that could be used to boost battery performances, reduce manufacturing costs, and reduce lithium use.

Source: Arcadium

Aluminum

Rio Tinto has also been a long-time producer of low-carbon aluminum, with hydropower providing the energy to refine bauxite into alumina and then aluminum.

Rio Tinto Overview

Overall, Rio Tinto is a global mining giant, providing investors with solid exposure to the iron market. It is also a green metal titan in the making, with aggressive moves made into copper and lithium, and maybe even gallium.

With technology to reduce iron ore emissions + already very low-emission aluminum production, it is well positioned to handle the emergence of any carbon tax on its products, giving it a potential competitive edge against its smaller competitors.